read white paper

October 2019

An 80% Climate Gas Reduction from Energy is Achievable by 2050 with Real Winners and Losers

Introduction

Climate change is an increasingly important topic for capital markets. It is not scaremongering to claim that this is the most pressing global issue this millennium. We have just passed a 1ºC global temperature rise, and at the current rate we will pass 2ºC in 40 years’ time. If we pass 2ºC there is a significant possibility we will reach 3-4ºC. Two degrees is viewed as the level triggering uncontrollable further rises, mainly due to large scale methane leakage as northern hemisphere permafrost starts melting on a grand scale. Limiting and controlling climate change is a requirement for continued peace and prosperity. Around three quarters of climate gases, mainly CO2 and methane, are caused by the extraction and burning of fossil fuels. Energy must therefore be at the forefront of any fixes.

Defining the Problem

The charts below show the contributors to the global greenhouse gas emissions whose main components are carbon dioxide (c.75%) and methane (16%). Around 70% of the total emissions balance is directly associated with the production and use of energy, with the remainder falling outside our scope of competence (agriculture, deforestation and similar).

Global Greenhouse Gas Emissions

Source: IEA

CO2 Emissions from Fossil Fuels

Source: IEA

In the following we assess the feasibility of achieving our target sector by sector, with the below starting points:

We target an 80% reduction of total CO2 emissions by 2050, consistent with preventing a 2ºC global temperature rise.

We are not assuming any technological breakthroughs, but using technologies and associated costs available today. The biggest challenge is in the industrial sector, where we need process changes to scale up from pilot stage to large scale to achieve the target.

We assume each subsector will reduce emissions by 80% to 2050. For oil and gas sector we assume a complete elimination of their methane and production related emissions, lowering the CO2 reduction from their production by 75%, achieving an 80% reduction in their products through managing a decline in oil and gas production.

Electricity (and Heat) Production – 41% of Total CO2 Emissions

The power sector is on track to achieve an 80% reduction in carbon emissions by 2050. This is not a distant scenario, it is the base case. Whilst it is still the largest emitter of climate gases, the carbon intensity has started to fall as a consequence of more than two thirds of net capacity additions going into renewables and an annual capex spend of US$200bn.

Renewable Investments Since 2011

Source: UN Environment, Bloomberg New Energy Finance

This base case requires current renewables capex to simply be maintained. This is conservative considering our assumption of 26% growth in global power demand by 2050, in line with population growth. Almost all current coal and oil plants will have come to the end of their useful life by 2050. We assume they get replaced by a mix of renewables and gas plants. Gas plants emit two thirds less CO2 than a coal plant. We model a doubling of gas generation capacity to ensure we have sufficient backup capacity when the wind does not blow and the sun does not shine, but we also assume these plants run at only a 30% average load factor, consistent with the role of swing/backup capacity.

The charts below shows how we foresee global power capacity and generation change by 2050. It should be noted the growth in installed capacity is steep as renewables only have about one third of the load factor of a thermal plant.

Installed Capacity Evolution from 2017 to 2050 (in TW)

Source: Internal analysis

However, this is not the entire message. The power sector will not only need to solve its own problems. Without science fiction level technological breakthroughs (such as fusion power) or large scale storage and removal of CO2 from the air, renewable generation will also have to contribute to the other sectors’ carbon challenges. We will need further large scale electrification which will require additional renewable capacity. We revisit this later in the section.

Buildings – 8% of Total CO2 Emissions

The building sector is not on track to lower its carbon footprint, and without concerted efforts we think it is unlikely to be achieved by 2050. Without regulatory or political change, our base case would be for stable emissions by 2050, with increased efficiency offsetting population growth. The challenge has very little to do with technology – you can fully electrify a house and in some more developed countries, such as Sweden, this is already the case. The main challenges are instead slow reinvestment cycles, lack of incentives and a large amount of extremely inefficient and polluting traditional energy use in poorer societies. An 80% reduction would be possible through energy efficiency and electrification of heating and cooking systems. Such a transition would increase renewable power generation volumes by c.5,000 TWh.

The below charts show the current distribution of the global building energy consumption and how the distribution would look in 2050 if one were to cut CO2 emissions by 80%.

Split of Building Energy Consumption by Source (%)

Source: UN Environment, Internal analysis

On average heating systems are replaced every 50 years when homeowners do a full refurbishment of a house. If current heating systems are replaced by heat pumps, energy savings of 60-80% can be achieved. However, it will take time and will require more capital intensive systems to be installed. Therefore, without measures speeding this up, savings will be slower and smaller. If direct heating was replaced by heat pumps on a global scale it would imply a large increase in electricity consumption, in the range of 3,000 TWh.

Cooking still represents 20% of buildings’ emissions. Whilst this is potentially surprising, we need to consider that most developing countries still cook over fires or very inefficient stoves. India, for example, uses firewood for 50% of the country’s cooking, and China relies on coal for 30%. Replacing these inefficient and polluting stoves with mainly electric alternatives would be one of the most efficient ways for buildings to lower emissions. On a 2050 time frame this could happen, as it has already in developed countries. This would imply another increase in the electricity consumption, which we estimate in the range of 500 TWh.

A new energy efficient house usually consumes around half the amount of energy of an older house, in extreme cases even less. Further insulating existing houses can often achieve 20-30% lower heat and cooling needs. However, this is usually a slow process, as changes to insulation also only take place when homeowners do a full refurbishment.

Industry – 24% of Total CO2 Emissions

Industrial carbon emissions have stabilised but are not yet on track for 80% decarbonisation by 2050. According to the IEA, industry direct emissions in 2017 were 8.5 Gt CO2, which can largely be explained by the use of coal and oil, as about half of the energy consumption was from these sources. With increasing ESG focus from investors, Industry has started to focus on innovations to help reduce emissions drastically. We note with interest Amazon’s recent carbon neutrality challenge. If this receives attention, industrials emissions would decrease quicker than the government mandates in many industries.

Within Industry, about half of the emissions comes from the cement, steel and chemicals sectors. These industry sectors are likely to get primary attention from ESG investors, as fossil fuel based heating could be replaced by clean energy based electricity. Hydrogen could also be playing a big role in terms of reducing the emissions from industry. Hydrogen has the capacity to replace methane in both production and heating processes. Industry would need to make changes to the chemical processes to get the emissions down 80% by 2050. Currently the costs of these new processes are certainly higher than for the traditional manufacturing processes. However, carbon regulations are increasingly being targeted to these industries. The analogy with the power sector is striking. Ten years ago very few would have thought that the power sector would be today on track to drastically reduce its carbon footprint. We thus believe industry can follow similar footsteps. Overall, we estimate that carbon emissions in the industry sector will decrease by 80% due to a combination of efficiency, change in fuel mix and change in the chemical processes. This would require about 15,000 TWh of additional renewable generation, according to our estimates.

Industry Direct Emissions (8.5Gt CO2 in 2017)

Source: IEA

Industry Energy Consumptions (156 EJ in 2017)

Source: IEA

Transport – 25% of Total CO2 Emissions

The transport sector is growing and almost fully dependent on fossil fuels, mainly oil. However, a combination of regulation and technological developments means we foresee a hockey stick change from here, making an 80% reduction in fossil fuel by 2050 within reach. Air transport is the challenge and will probably have to take a larger share of the carbon budget. This will, however, require a massive step up in the use of power and alternative fuels. Reducing 80% of transport emissions would require 16,000 TWh of new renewable power generation.

The transport sector currently consumes 60% of global oil. Two thirds of which is due to road transportation, while the remaining third is mainly consumed by airlines and ships. The sector is likely to continue to experience growth, mainly driven by emerging markets and aviation. We forecast an 82% increase in transport volumes by 2050. However, things are set to change. We believe an 80% reduction in carbon emissions by 2050 is a likely base case, due to a combination of much higher efficiencies and moving away from hydrocarbons as a consumable fuel.

The growth in transport demand is likely to be almost entirely offset by continued gradual increase in energy efficiency, particularly in light and heavy duty vehicles, where technologies, such as brake energy recuperation, enable large savings.

To reach the target, the industry will also need a large shift away from internal combustion engines, towards battery electric and hydrogen powered vehicles. For light duty vehicles, electric cars are already commercially available, and in Norway already more than 50% of new car sales are fully electric. For heavy duty trucks and buses, batteries can effectively be utilised within cities. For long distance trucking, as well as marine, we expect hydrogen will be a more cost efficient solution. For aerospace, batteries are not a realistic solution beyond regional flights due to their low energy density. We expect biofuels and synthetic eFuels will be necessary to offset emissions. Conventional jet fuel is, however, still expected to be widely used in many regions in 2050. Our technology assumptions required to hit an 80% reduction in CO2 emissions are listed in the table below.

The targets might sound ambitious today, but, in our view, with political support they are very feasible. In the case of road transportation, total ownership cost will be reduced, while shipping and airlines will likely need to pay fuel taxes on similar levels to that of cars and trucks. In terms of resources, the targets are also feasible. For biofuels we only need 3% annual production growth through 2050, ending up with a production of slightly more than double what we have today. However, the consumption of biofuels has to be redistributed from cars to airplanes and ships. Hydrogen does not require any particularly rare materials, as latest generation fuel cells do not require more platinum than regular diesel catalysts. Developing the battery industry will require investments, but the raw material limitations are probably overstated.

By 2050 we see the need for around 4,000 GWh of battery manufacturing, up 16x vs today’s production. While this sounds dramatic, it only requires a capex requirement of US$20-25bn per year, around 10% of the automotive industry capex spend today. For raw materials, such as lithium and cobalt, the growth requirement would be even less, as the industry, similar to solar, is seeing constant year over year improvements in energy density. For cobalt there is a real risk the material will be replaced by nickel and cobalt demand will peak by 2030. Both lithium and cobalt are today in serious oversupply, and hence we think lithium mining capacity will only need to increase 4x by 2050.

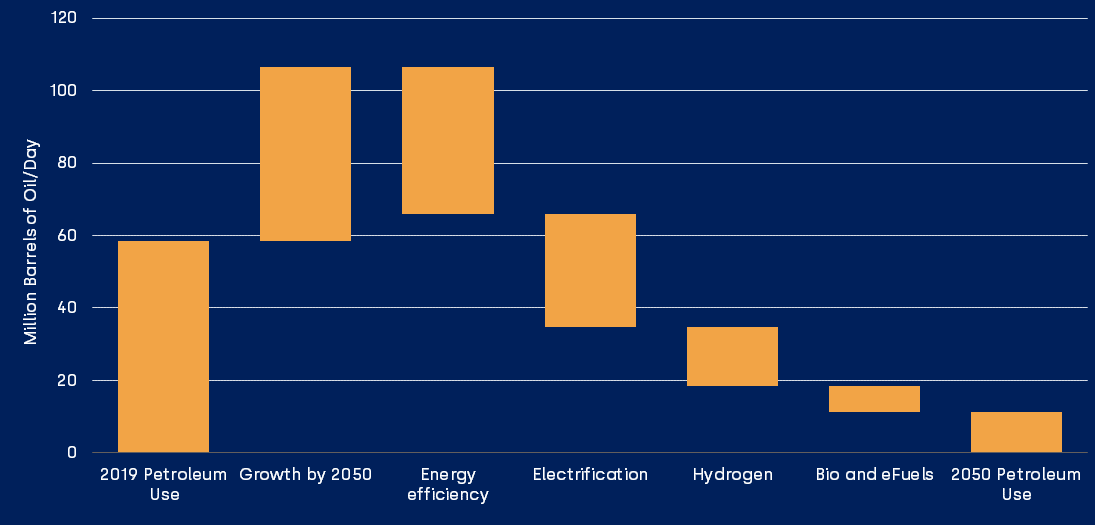

The chart below shows our route to an 80% oil demand reduction in Transport. Increased efficiency will accomplish almost half of the required reduction, with electricity and alternative fuels having similar shares accomplishing the objectives.

Road to Sustainable Transportation

Source: Internal analysis

The Total Power Sector Challenge

Having gone through different sectors we conclude that increased use of electricity is the main, and currently available, way to limit climate gases. Thus, the power sector is likely to show very substantial growth in a low carbon future. The chart below shows the different building blocks needed to achieve an 80% reduction in carbon emissions in energy related sectors. We estimate the yearly capex needed to accomplish this build out would be US$500bn per year. The current utility and oil and gas industries, with no public sources or subsidies, could accomplish this, if this was their primary focus.

Incremental Electricity Demand from Decarbonising Power, Buildings, Transport and Industrial Sectors

Source: Internal analysis

Therefore, this is financially quite possible, but is there space? The answer is again, definitely. If we assume future capacity to be 50% solar, 30% onshore wind and 20% offshore wind we would need 1 million km2 of land, less than 0.7% of global surface area, and 0.7 million km2 of shallow sea bed. Space is not an issue.

80% CO2 Reduction by 2050 Would Only Require 0.7% of World Land Area for Renewables Power Generation

Source: Internal analysis

Conclusions

We have assessed how realistic an 80% reduction target would be for energy related climate gases by 2050. The conclusions are surprising and more encouraging than we thought:

Power remains the largest carbon emitter, but has seen a huge increase in renewables deployment over the last 5-10 years. It is on track to achieve the reduction target if it continues to invest with the current intensity. Also, as power is the dominant user, thermal coal should mostly be eliminated by 2050.

Industry and Buildings are not on track. The technologies needed are available but deployment must speed up. We are more optimistic for industry to be able achieve our 80% target than buildings. While progress to date has been slow, a combination of commercial forces and regulation, e.g. carbon pricing, could drive rapid decarbonisation in industry. For buildings technological solutions are straightforward, with electric cooking and heating used in many regions today. The barrier is consumer bills. Financial support will likely be needed to incentivise a shift to more expensive heating sources.

The Transport sector is not on track. The sector is almost entirely reliant on fossil fuels, mainly oil, and shows the quickest emission growth. Air and shipping remain challenging areas. We would also need to see a transfer from air to rail for short to medium range transport. However, in our view we are at the beginning of a real hockey stick with widespread electrification and alternative fuels for road transport. Transportation already has extremely strong political support, with firm regulation in place to decarbonise in the most important markets.

To achieve an 80% reduction in energy related climate gases we would need to see increased electrification of energy use for transport, industry and housing. We estimate this fuel switch would require US$23trillion or US$760bn of annual capex per year on a global scale. A staggering sum, but in fact broadly in line with annual oil and gas industry capex. The industry reallocating all its growth capex and free cash flow (assuming prevailing oil and gas prices) to renewables would finance most of the gap out to 2050 (as our RDS case study shows).

To conclude that there is a future for the oil and gas sector in a carbon constrained world is both surprising and positive to us, in light of an increasing ESG sentiment headwind for the sector. The majors have the balance sheets and cash flow to be a big part of the transition and therefore the solution. This will require bold decisions to be taken. If they are not, investors should continue to shun the industry.